Know law deeply

Fight fearlessly.

✦ CS K K Agrawal ✦

✦ CS K K Agrawal ✦

Step by step guide to

Master Tax Litigation

Know Law Deeply | Fight Fearlessly

GST

Income Tax

Resources

Taxbykk ai

About Expert faculty

KK Agrawal

K K Agrawal is a seasoned GST and Income Tax Litigation Practitioner with over 25 years of dedicated experience in handling complex tax disputes across India.

About KK Agrawal

K K Agrawal is a seasoned GST and Income Tax Litigation Practitioner with over 25 years of dedicated experience in handling complex and high-stake tax disputes across India.

His professional journey is rooted in strategic tax advocacy from issuance of notice to Supreme Court litigation preparation.

Philosophy: KNOW LAW DEEPLY, FIGHT FEARLESSLY.

Faculty Member at NACIN, Taxmann Author, Founder of TaxByKK.com & Creator of TaxByKK.ai.

Mentoring tax professionals across India through TaxByKK.org.

♟Step 1 - Live Discussion Club

GST Premium Discussion Club

Know Law Deeply, Fight Fearlessly with + 40 members and grow your GST litigation practice

🎞️ Step 2 - Recorded Sessions

₹ 239

₹ 359

₹ 479

₹ 599

₹ 799

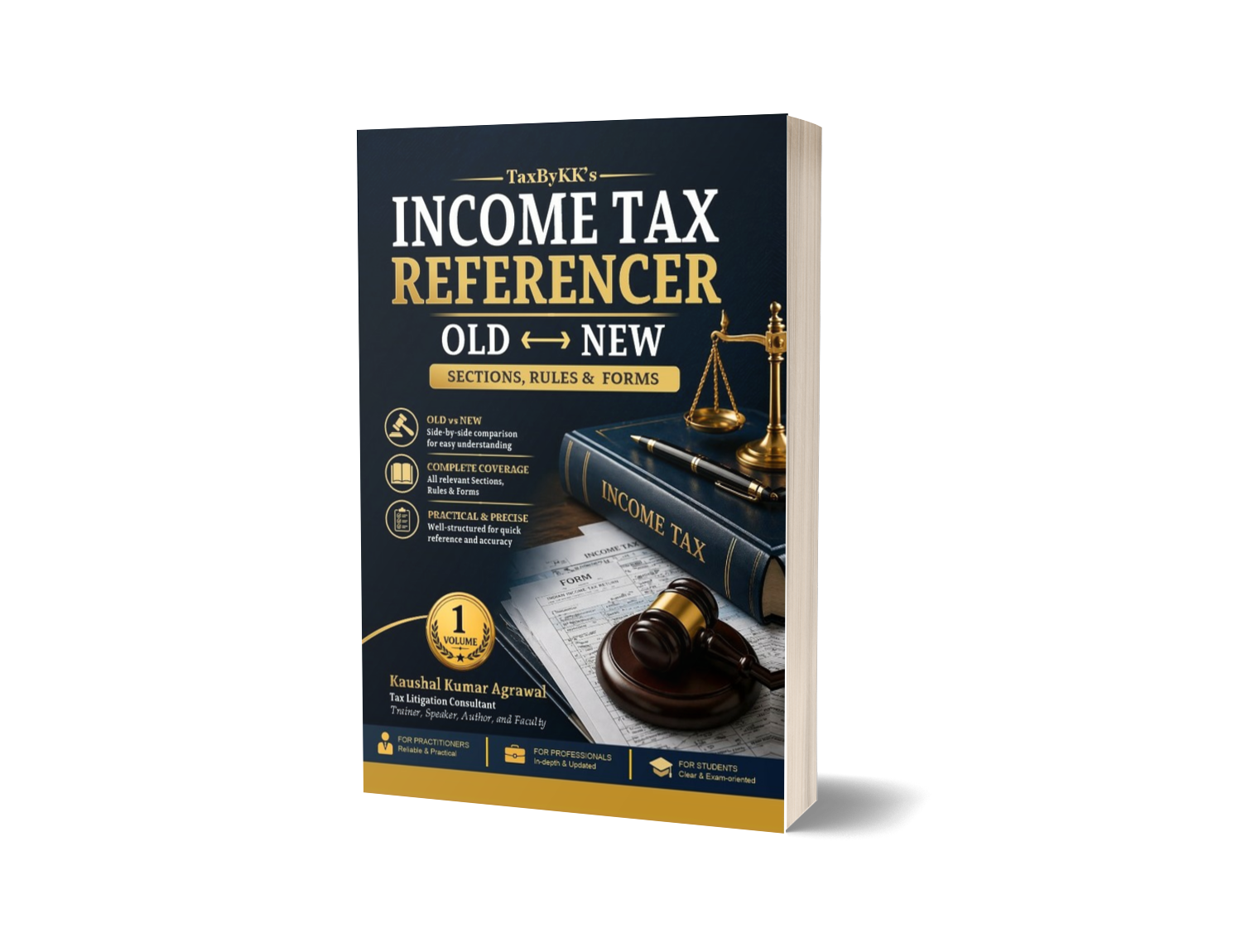

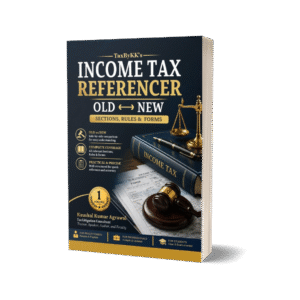

📚 Step 3 - Our Best Sellers

♟Step 4- Live Litigation Club

GST Premium Litigation Club

Know Law Deeply, Fight Fearlessly,

Live Discussion of your GST Notices & Queries

🏛️ Step 5 - GSTAT Club

GST Premium

GSTAT Club

Where TaxByKK (TBK) Premium Members Learn, Grow & Collaborate in GST Practice

Visit Now